12 of 16 U.S. Nonresidential PIP Building Groups in the Pink

A Sharp Divide in the Construction Marketplace

The ‘duality’ theme usually ascribed to the economic climate these days—e.g., on the net retail profits ‘great’ vs ‘bricks and mortar’ retail income ‘struggling’—since the onset of the coronavirus pandemic can also be utilized to the nation’s development market.

The Census Bureau’s 2020 stop-of-year data on put-in-position expenditure in the U.S. confirmed complete dollar volume getting +4.7% when as opposed with the full of 2019. But the expansion was solely in residential development, +11.8%, whilst nonresidential stayed flat, -.1%.

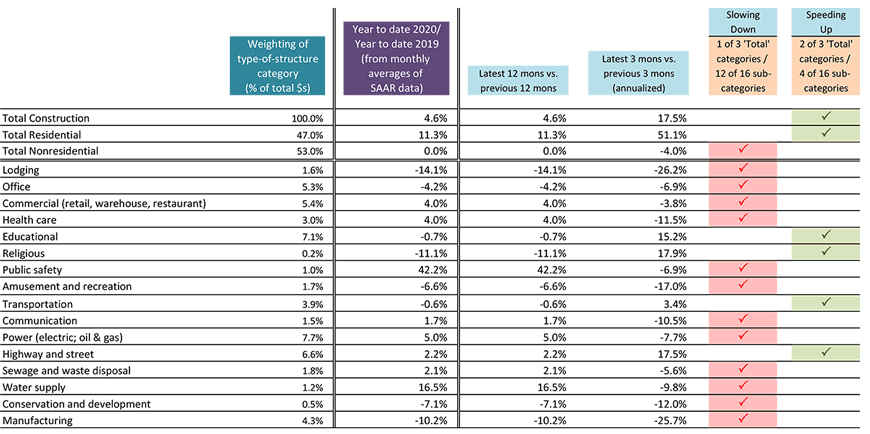

Desk 1 sets out numbers, derived from the every month PIP info, that highlight the disparity involving residential and nonresidential operate a lot more obviously (and as a result, far more alarmingly).

To set up no matter whether paying in a selected sort of design class has currently been ‘speeding up’ or ‘slowing down,’ Desk 1 compares most recent-three-months more than prior-a few-months performances (annualized) in opposition to most current-12-months over prior-12-months.

If the previous yields a proportion modify greater than the latter, then it is assessed to be an instance of ‘speeding up’ and a verify mark is positioned in the considerably-proper column of the desk. If the reverse is legitimate, then it is considered to be a scenario of ‘slowing down,’ earning a examine mark in the next-to-remaining column.

For this exercise, when a unfavorable modify gets fewer negative, it is awarded a look at mark in the ‘speeding up’ column. When a adverse goes further into the gap, it receives a test mark in the ‘slowing down’ column.

As a sidebar, for December of any 12 months (which is the thirty day period currently being scrutinized in this post), the proportion alter figures in the ‘year to date’ and ‘latest 12 months’ columns are the identical.

A Boom in Residential Design Activity

In Desk 1, the ‘total’ worth of design in December 2020 was ‘speeding up,’ heading from +4.6% to +17.5%. But look at the two primary components. Residential was the obvious driver, accelerating from +11.3% to +51.1%. The fourth quarter of very last year noticed a half-once more pickup (annualized) in residential design shelling out in comparison with the third quarter.

What is not obvious from the Census Bureau’s figures is how a lot of the current get in residential design action has been from new assignments (i.e., homebuilding) as opposed to renovation do the job. Groundbreakings on new single-household residences have been soaring of late, but ‘working from home’ has also offered a significant incentive to proceed with reworking initiatives.

Curiously, ‘residential’ grabbed a a lot much larger share of ‘total’ in December 2020, at 47%, than in December 2019, 41%. Nonresidential construction’s share of the ‘total’ volume of design correspondingly diminished to 53% from 59%.

Nonresidential Design Pausing & Considering

By the close of previous calendar year, money spending on nonresidential development, as a entire, was ‘slowing down,’ transferring from .% for newest-12-months transform (or absence thereof) to -4.% for most up-to-date-three-months improve.

Far more drastically, funds paying out in 12 of nonresidential’s 16 form-of-composition subcategories possibly softened or softened more. The most noteworthy pullbacks occurred in: lodging, from -14.1% to -26.2% communication, from +1.7% to -10.5% energy, +5.% to -7.7% health care, +4.% to -11.5% producing, -10.2% to -25.7% drinking water provide, +16.5% to -9.8% and community security, +42.2% to -6.9%.

The electric power and producing subcategories had been vulnerable to the winding down of perform on mega-measurement vitality initiatives that had been initiated in 2019, ahead of the coronavirus beachhead was founded.

Desk 1 does emphasize four subcategories of nonresidential design with check out marks in the ‘speeding up’ column. ‘Religious’ in December held up +17.9% for most recent-a few-months to distinction with -11.1% for hottest-12-months, but its share of ‘total’ was a minimal .2%.

Additional encouraging developments had been to be discovered in academic development, from -.7% to +15.2% transportation, -.6% to +3.4% and highways and streets, +2.2% to +17.5%.

Roadwork further expending relates to new suburbs that are remaining eco-friendly-lighted. Additionally, there are potential customers for a lot extra perform to come if the recently set up Democrat administration in Washington functions on its election guarantee of a large infrastructure shelling out monthly bill. Pete Buttigieg, in his new part as Secretary of Transportation, ought to be itching to start this kind of an initiative.

The university investment is to make training institutions safer, from a wellbeing standpoint, for returning pupils.

In ‘transportation,’ many massive metropolitan regions have big LRT and subway expansions on their drawing boards. Timing of all those jobs, although, appears open to question, specified the tough COVID-19-relevant financial conditions that have landed on city council doorsteps.

Table 1: U.S. Put-in-location Development Investment decision − December 2020

Based on ‘current’ (i.e., not altered for inflation) $s, seasonally altered at yearly costs (SAAR)

In the ultimate two columns, if there is no check mark in the cell, then the type-of-composition category has stayed in just 1.%, up or down.

A adverse that becomes much more destructive is deemed to be ‘slowing down’ if significantly less unfavorable, then ‘speeding up’.

Facts source: Census Bureau / Desk: ConstructConnect