Lowe’s Inventory Undervalued When compared To Household Depot?

NEW JERSEY, UNITED STATES – 2018/02/15: Lowe’s house improvement superstore. (Photograph by John … [+]

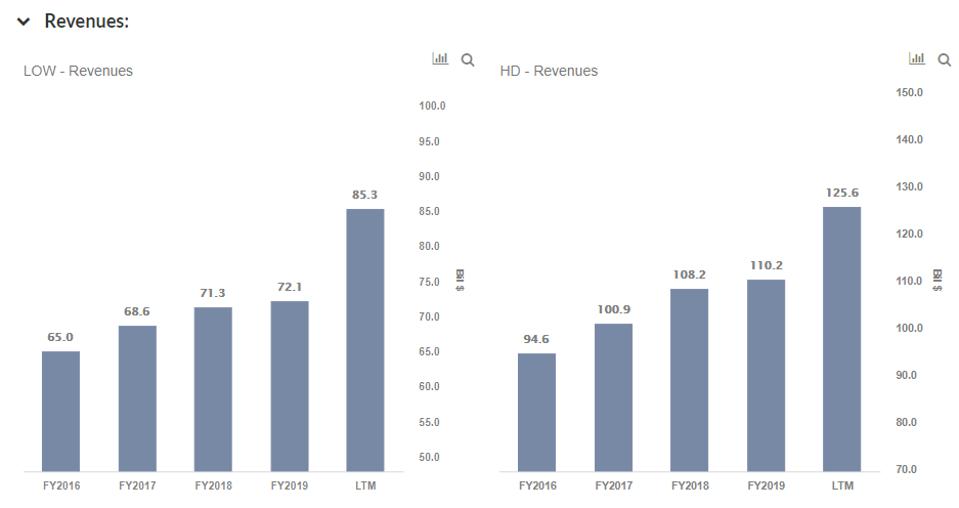

Both of those home enhancement suppliers in the U.S, Lowe’s (NYSE: Reduced) and House Depot (NYSE: High definition), are riding high on the Covid-19 wave as clients spent additional of their disposable cash on house enhancement assignments instead than on holidays or eating out. But is Lowe’s inventory appropriately priced compared to House Depot inventory? We feel that Lowe’s inventory is incredibly undervalued when compared to Hd stock, owing to the noteworthy mismatch in their current P/S multiples when as opposed with revenue growth and running margins for the two firms around the latest several years. Lowe’s P/S a number of of 1.5x is substantially decreased than the determine of 2.3x for Home Depot.

Lowe’s earnings development about the previous twelve months improved by 18.9%, which was better than the determine of 13.2% for Residence Depot. During the similar period of time, the working margin for Lowe’s transformed by 2.7 proportion details, once more greater than the improve of -.3 percentage factors for House Depot. Our dashboard Lowe’s vs. Household Depot: Minimal stock seems extremely undervalued in contrast to High definition inventory particulars the total picture centered on earnings advancement and operating margin – sections of which are summarized beneath.

1. Earnings Growth

Even though Residence Depot however generates 1.5x a lot more revenues than Lowe’s, the latter’s earnings expansion was bigger about the last 12 months in 2020 (19% vs 13% for Hd).

- Of training course, the odds of either retailer sustaining their current degrees of expansion write-up-Covid are slender. But Lowe’s nevertheless has a great deal of space to grow, offered its the latest e-commerce enhancements. Lowe’s Full House strategy is an encouraging advancement that sets the phase for this risk. The initiative aims to enrich shopper engagement and develop market place share.

- Likely forward, Lowe’s bigger target on its skilled contractor people is offering a enhance that could outlast the existing home owner demand.

2. Operating Income

Coming to working revenue, Lowe’s had a apparent edge around House Depot in the very last a single 12 months.

- Lowe’s functioning margin was 8.4% for the most modern twelve-thirty day period interval, which is lower than Property Depot’s functioning margin of 14.1%

- More than the final twelve months, the running margin for Lowe’s improved by 2.7 pp (share details) – far better than the improve of -.3 pp for House Depot

- In the nine months of fiscal 2020 so considerably, Lowe’s exact-keep sales progress of 26% in the U.S. prompted a 52% yr-in excess of-year advancement in running income. Household Depot’s identical-retailer gross sales were being only up 18% for the identical interval, prompting a a lot more modest 14% maximize in running gains.

The net of it all

In summary, the net gain moves again to Lowe’s based mostly on its bigger profits expansion and far better working cash flow growth in the latest scenario as when compared to House Depot. While Household Depot is even now far more profitable, Lowe’s inventory has performed improved in 2020. Lowe’s and Dwelling Depot trade at an just about similar 2x projected 2021 Profits. In addition, Lowe’s shares are investing at 17 times believed FY 2021 earnings, and Household Depot trades at 22 moments the exact estimates relative to projected earnings.

Although Lowe’s stock is really worth taking into consideration, 2020 has developed lots of pricing discontinuities that can offer beautiful investing alternatives. For example, you will be shocked how counter-intuitive the stock valuation is for Amazon vs Etsy.

See all Trefis Cost Estimates and Download Trefis Info here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Groups | Products, R&D, and Internet marketing Groups